Key Findings At a Glance

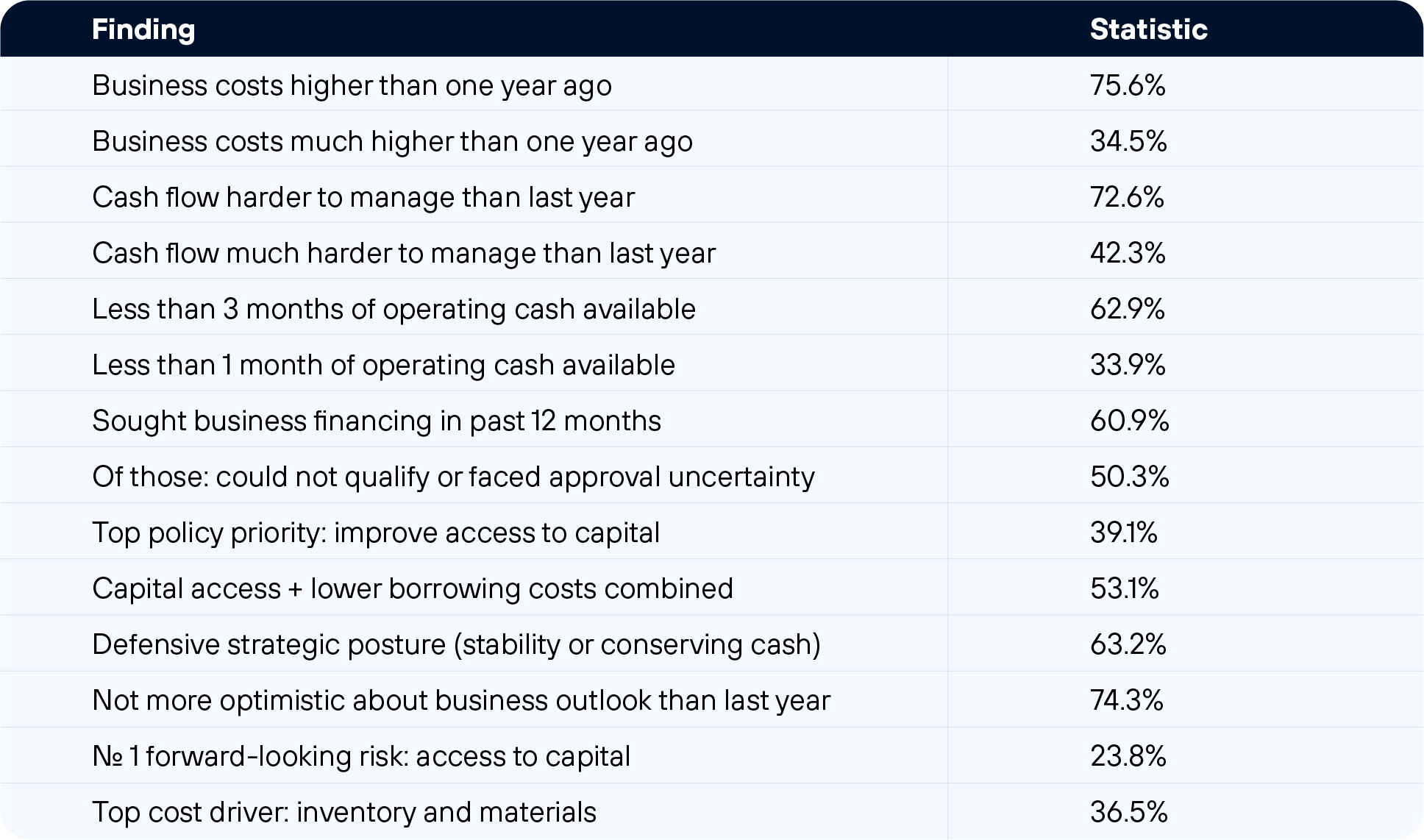

• 75.6% of small business owners say costs are higher than a year ago; 34.5% say much higher

• 72.6% say cash flow is harder to manage than last year; 42.3% say much harder • 62.9% have less than three months of operating cash if revenue slows; 33.9% have less than one month

• 60.9% sought financing in the past 12 months; of those, 50.3% could not qualify or faced uncertainty of approval

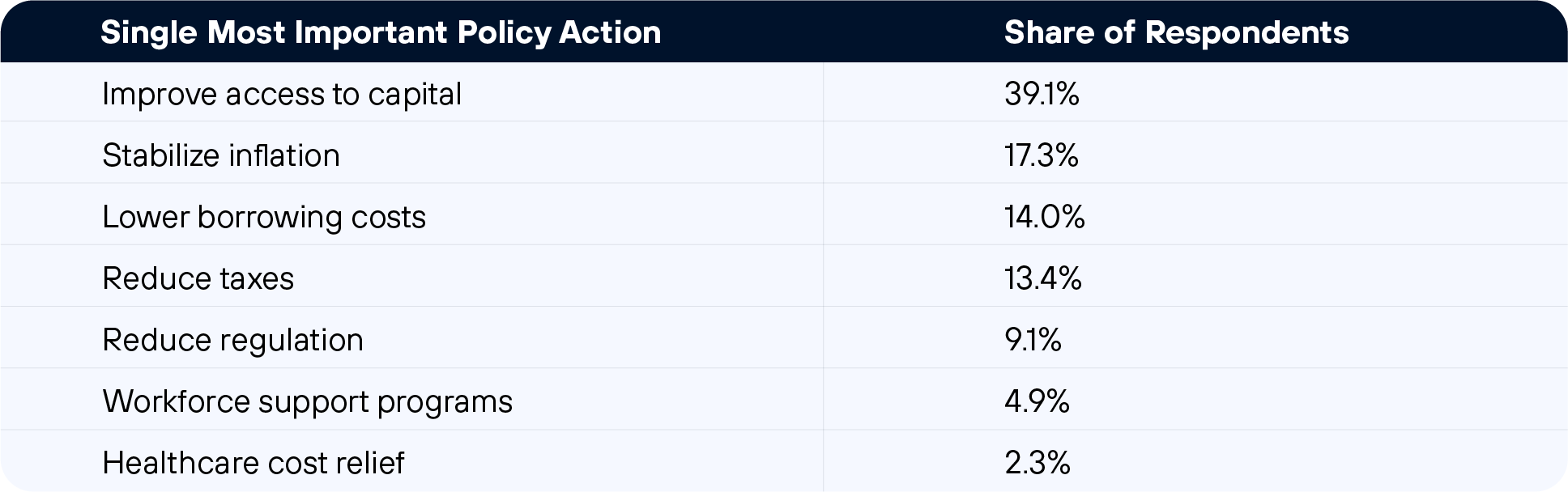

• 39.1% say improving access to capital is the single most important policy action available to policymakers

• 63.2% are operating in a defensive posture: focused on stability or actively conserving cash

Executive Summary

Small business owners across the United States entered 2026 facing persistent and broad-based economic pressure. Three in four report that business costs are higher today than they were a year ago. Nearly two-thirds have fewer than three months of operating cash if revenues slow. Among the 61 percent who sought financing in the past year, more than half were turned away or left uncertain about whether they would qualify.

Those findings come from a survey of 307 small business owners and operators conducted by Revenued in February 2026. Respondents were drawn from three groups: existing Revenued accountholders (n=68), recent applicants who were not approved for funding (n=125), and prospective leads who had not yet applied (n=114). A separate 18-person pulse survey on tariff policy reactions was fielded in the same period.

The data does not describe businesses in passive decline. Owners are cutting costs, raising prices, drawing down savings, and deferring expansion. They are making deliberate, often painful tradeoffs to stay solvent. But the frequency and intensity of those tradeoffs point to structural gaps in the small business financing system that are limiting their ability to stabilize and grow.

This report presents findings across five areas: cost pressure, cash reserves and cash flow, access to capital, business outlook and strategy, and tariff policy impact. Verbatim responses from participants who provided public attribution consent are included throughout.

Methodology

This report is based on two surveys conducted by Revenued, a U.S.-based financial technology company, in February 2026. The primary survey was distributed to three segments: funded accountholders (n=68), applicants who were not approved (n=125), and prospective leads who had not yet applied (n=114), for a combined total of 307 respondents. A supplemental pulse survey on tariff policy reactions was separately administered to 18 respondents during the same period, following news of potential tariff policy changes.

The survey was administered online. Respondents received a gift card incentive of up to $25 for their participation. All reported percentages reflect the combined three-segment total unless otherwise noted. Verbatim quotes are drawn only from respondents who expressly granted public attribution consent. The tariff pulse survey (n=18) is treated as qualitative and directional; it is not used to generate headline statistics. This research was commissioned and conducted by Revenued for publication purposes. Revenued provides revenue-based business funding products. This report does not constitute financial or legal advice.

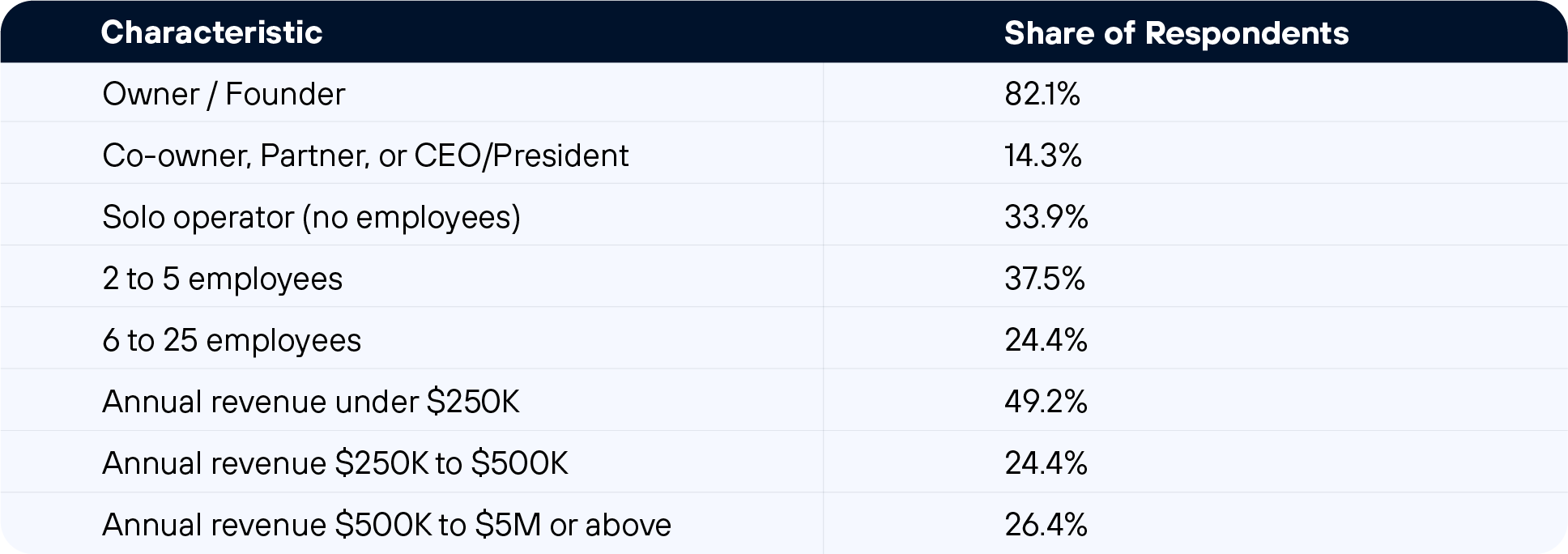

Respondent Profile

The respondent pool reflects the small business owner Revenued most commonly serves. Nearly 90% identified as Owner/Founder, Co-owner, or CEO/President. More than 96% reported their business as actively operating at the time of the survey.

Business size skewed small. One-third of respondents are solo operators with no employees. Another 37.5% employ between two and five people. Nearly half reported annual revenue under $250,000. The top industries represented were Professional Services (22.1%), Retail/Ecommerce (16.6%), Construction and Trades (15.6%), Healthcare and Wellness (8.8%), Transportation and Logistics (7.2%), and Restaurant and Food Service (6.2%).

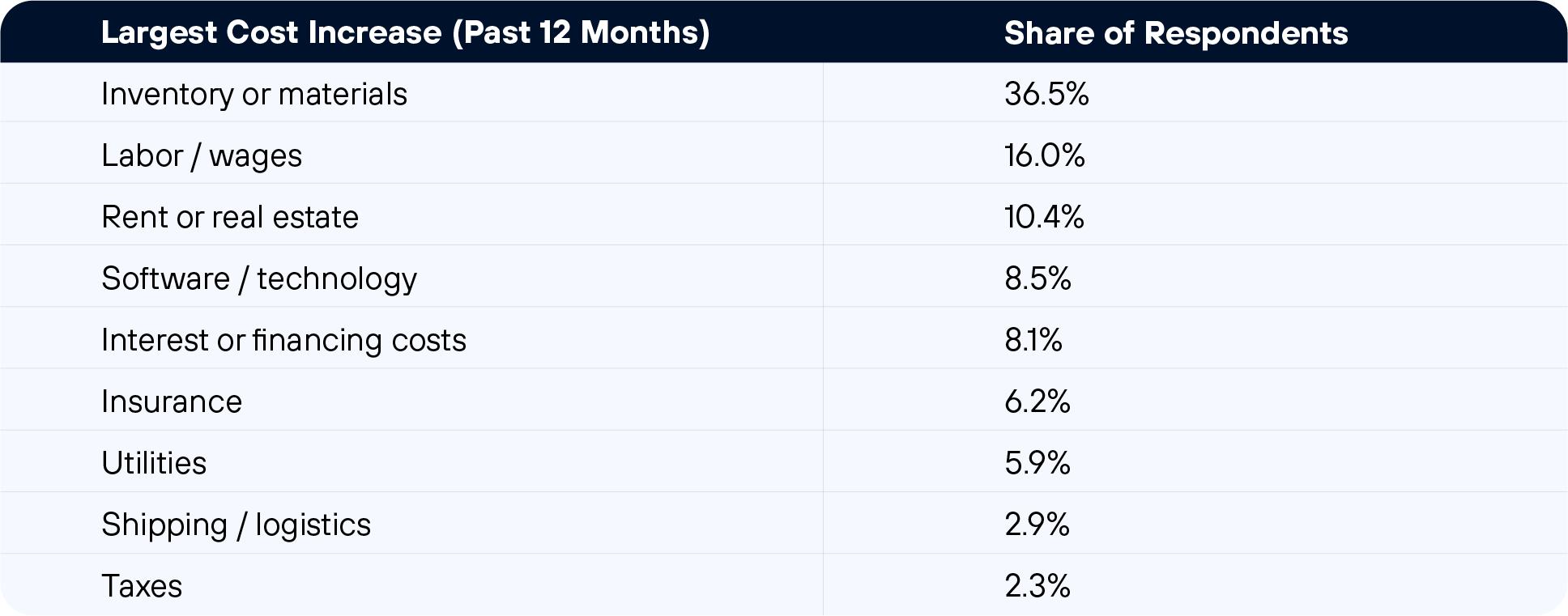

Section 1: Cost Pressure

Where Costs Are Rising

Unlike an inflationary environment driven by a single input category, the current cost pressure is distributed across nearly every line of the income statement. That breadth makes it harder to respond through any single operational change, and it limits the degree to which raising prices in one area can offset costs rising across several others.

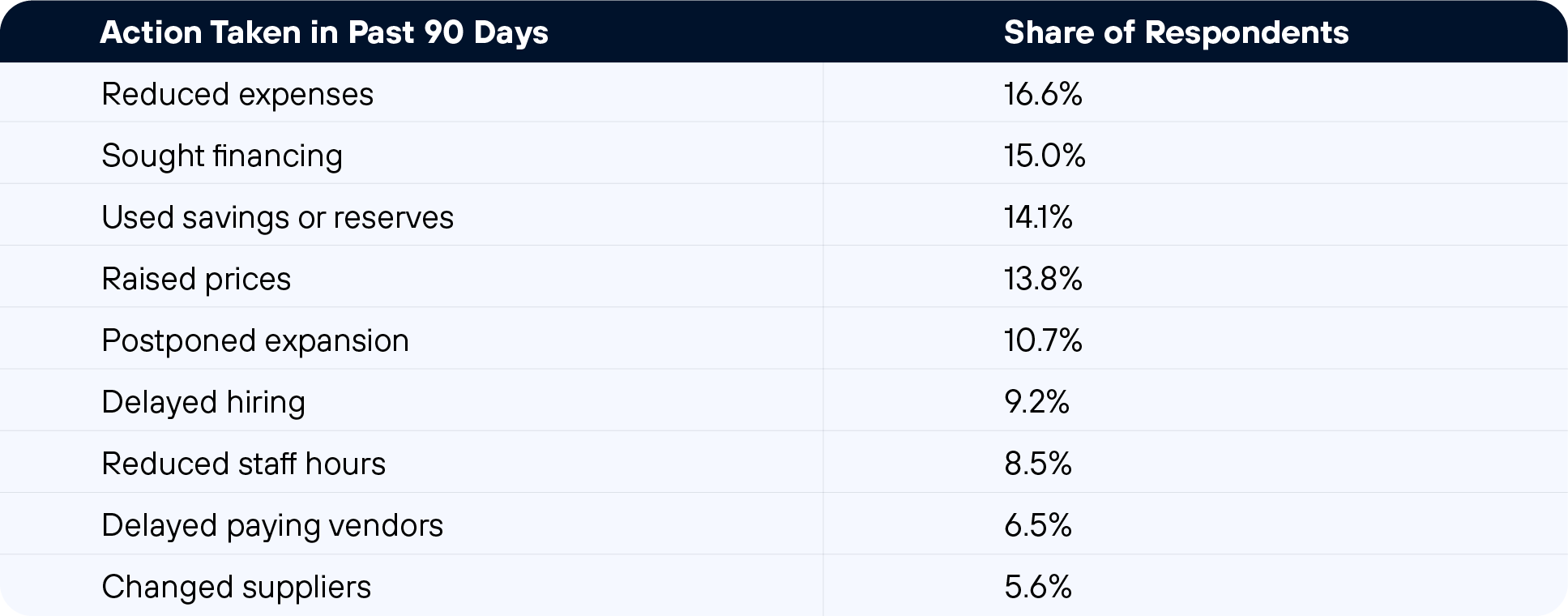

Actions Taken in Response

Over the 90 days prior to the survey, respondents reported taking a broad range of actions to manage rising costs. No single response dominates the distribution, which itself is instructive: owners are pulling multiple levers at once rather than relying on any one approach.

Both "sought financing" (15.0%) and "used savings or reserves" (14.1%) rank among the top four responses. That combination points to a population that is already drawing down existing capital to meet current operating costs.

Survey respondent, retail sector

“I can’t pass along all of the increased pricing and tariffs because my clients wouldn’t purchase from me; I end up absorbing a lot.”

Survey respondent

“Everything is more expensive than just one year ago. It’s getting harder and harder to keep people employed.”

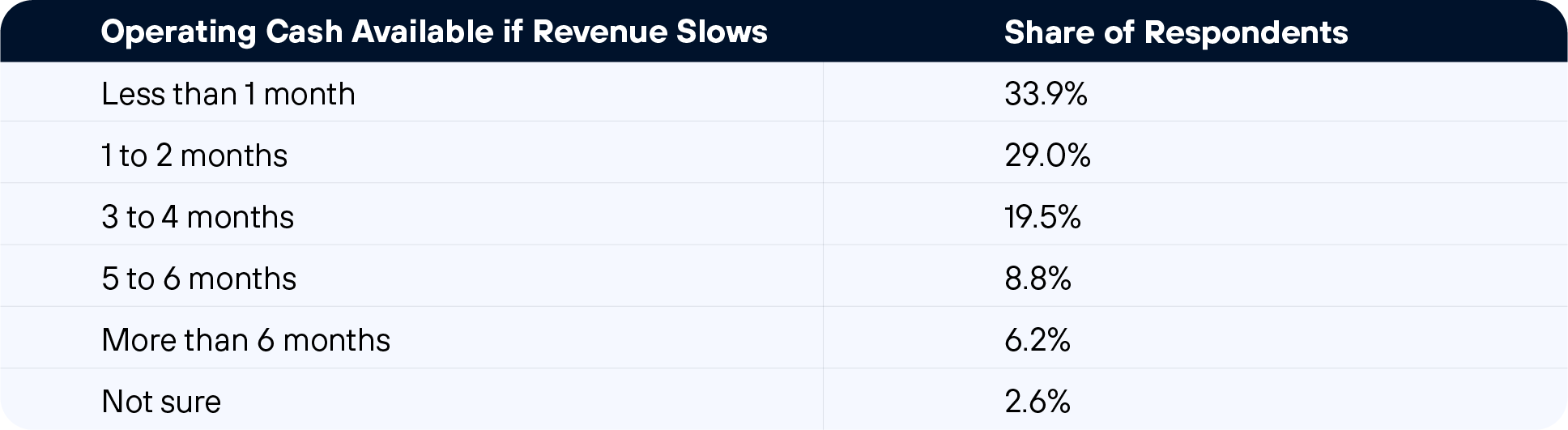

Section 2: Cash Reserves and Cash Flow

Cost pressure describes the force hitting these businesses. Cash reserves describe the cushion available to absorb it. By that measure, most small business owners in this survey have very little room to maneuver

Cash Runway

When asked how many months of operating cash their business currently has available if revenue slowed, one-third of respondents said less than one month. Another 29.0 percent said one to two months. Combined, 62.9 percent of respondents have fewer than 90 days of runway.

Only 6.2 percent of respondents have more than six months of reserves. A disruption of any kind, a slow quarter, a delayed client payment, an equipment failure, puts the businesses in the bottom third of this distribution at immediate risk.

This pattern held across all three respondent groups, including funded accountholders. It appears to reflect a structural reality of operating a small business at this scale, not just the profile of applicants who were declined.

Cash Flow Difficulty

72.6 percent of respondents say managing month-to-month cash flow feels harder today than it did a year ago. Of that group, 42.3 percent chose the most extreme available response: much harder. Only 4.9 percent say cash flow has become easier.

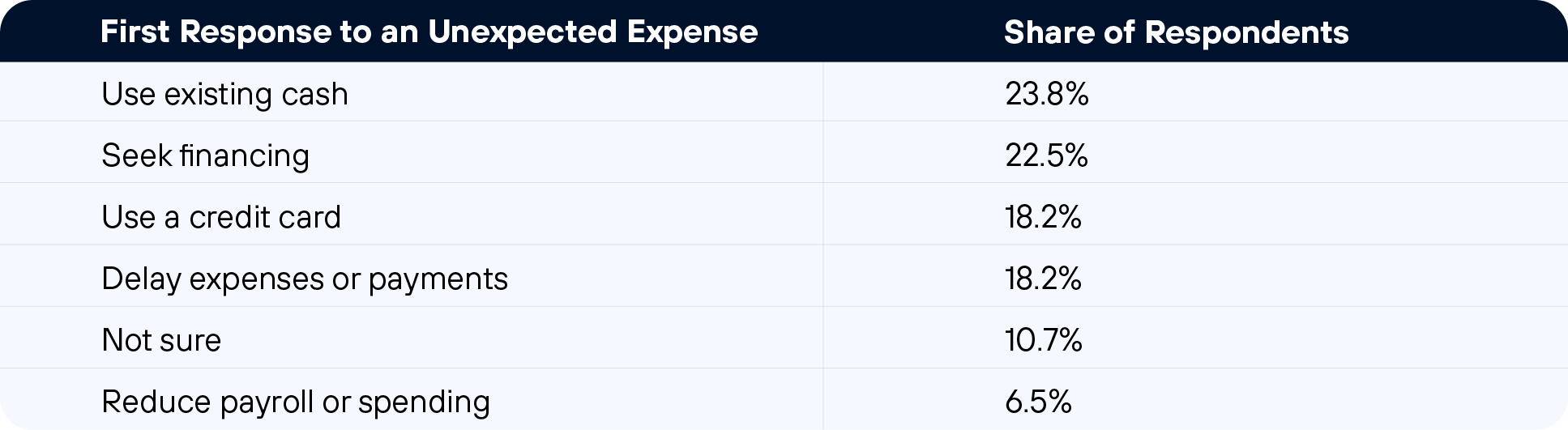

Responding to Unexpected Expenses

76.2% of respondents, by their own account, do not have the cash to absorb an unexpected expense from existing reserves. They would need to borrow, defer, or improvise.

Survey respondent

“They all think we have a ton of cash when in reality we have credit card payments and stress.”

Survey respondent

“It’s so hard. If I don’t work, I don’t eat. That simple.”

Section 3: Access To Capital

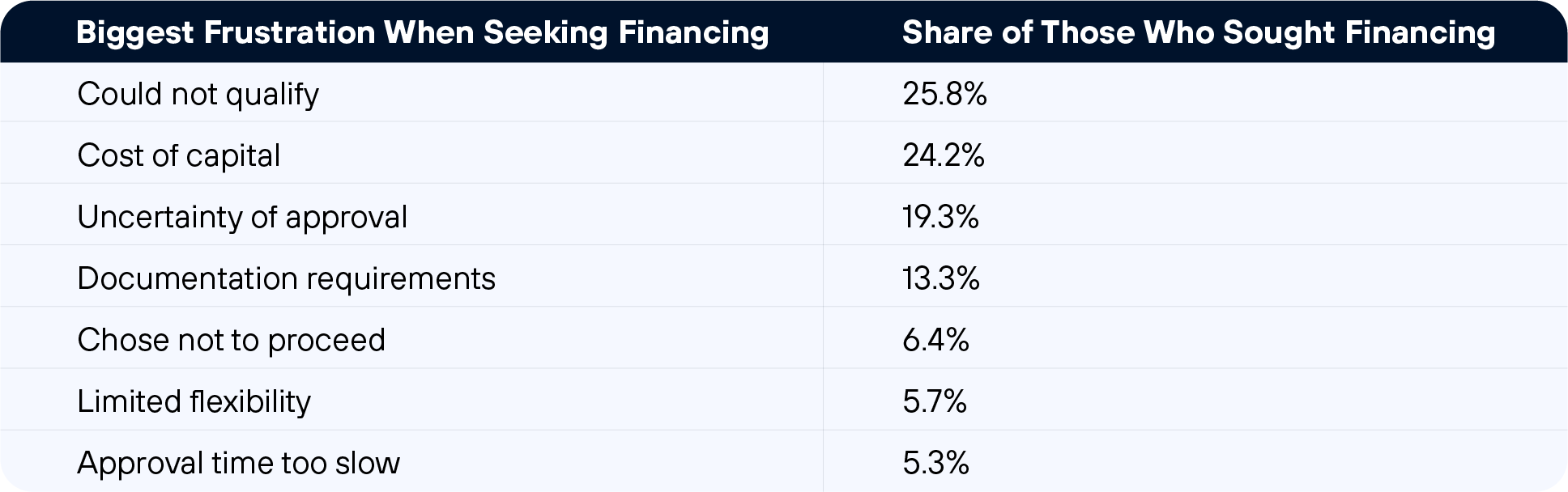

Financing Frustrations

Among respondents who sought financing and cited a frustration, inability to qualify ranked first at 25.8 percent. Cost of capital ranked second at 24.2 percent, followed by uncertainty of approval at 19.3 percent and documentation requirements at 13.3 percent

The two leading frustrations, inability to qualify and cost of capital, point to structural rather than administrative barriers. This is not primarily a problem of paperwork or processing time. The more common obstacle is either failing to meet eligibility standards or finding that the available capital is too expensive to justify

Capital Access as the Top Policy Priority

Survey respondent

“I think the aspect of having access to capital is misunderstood the most right now. The second aspect that is misunderstood is the difficulties we face balancing growth and quality.”

Survey respondent

“Those of us with newer businesses and good business credit but not good personal credit get screwed because no one thinks about the fact that we ruined our personal credit to get the business going.”

Survey respondent

“A small business can be doing everything right and still struggle without affordable funding and predictable expenses.”

Section 4: Economic Outlook and Business Strategy

Business Outlook Compared to One Year Ago

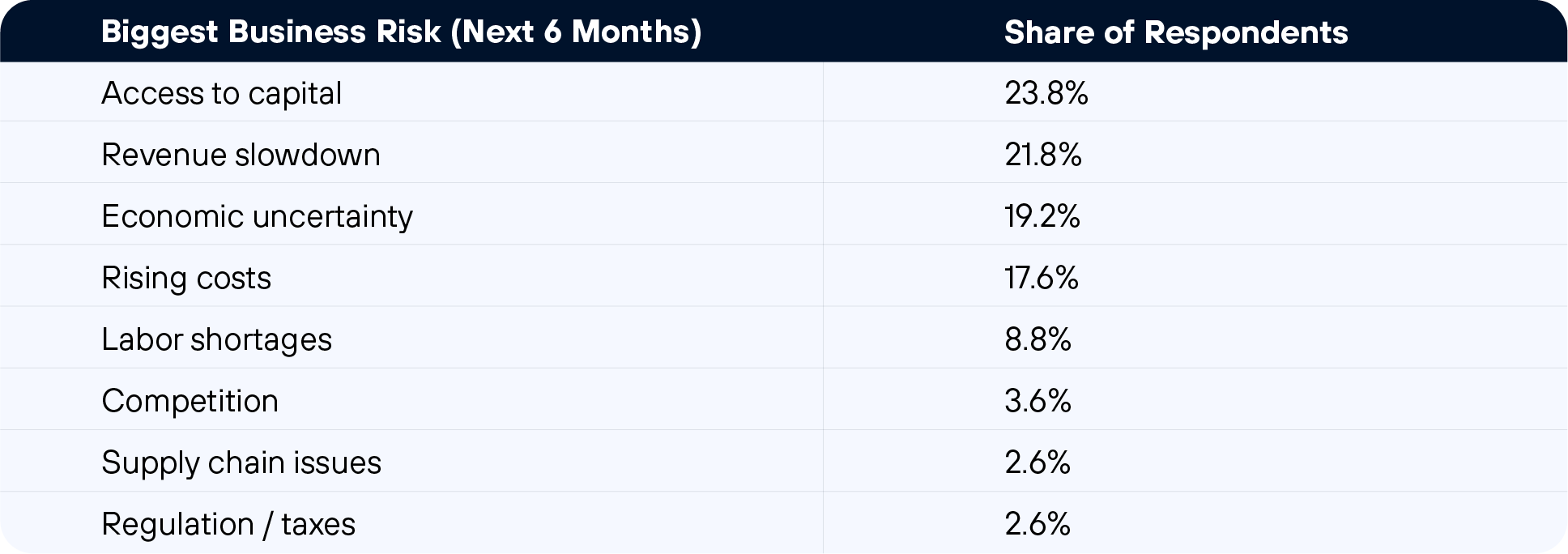

Biggest Risks Over the Next Six Months

What Business Owners Are Delaying

Open-ended responses to the question "What is one decision you delayed or changed recently because of economic pressure?" produced a consistent picture across all three respondent groups. Expansion decisions appear most often: new locations, additional hires, equipment purchases, fleet additions, and new product lines that were planned but have been put on hold. A second group of responses describes operational retreats, including reduced marketing spend, deferred vendor payments, shortened business hours, and in several cases, temporarily suspending operations entirely.

A third category involves personal financial sacrifice. Respondents cited cancelled family vacations, delayed home purchases, and second jobs taken to support the business. For most owners surveyed, the business and personal finances are not separate budgets.

Survey respondent

“We have delayed expansion. It is too risky given the state of our economy. We cannot guarantee success, but the risk does not outweigh the possible reward.”

Survey respondent

“I delayed hiring support staff and opening a physical office space, choosing instead to operate lean and remote until revenue becomes more consistent.”

Survey respondent

“I recently delayed expanding because the economy is unpredictable. Growth is exciting, but right now protecting cash flow and staying lean makes more sense than scaling just to say I did.”

Section 5: Tariff Policy

Note: This section is based on a separate rapid-response pulse survey of 18 respondents, fielded in February 2026 following news of potential U.S. tariff policy changes. Due to the small sample size, findings here are presented as qualitative and directional only. They are not intended to be statistically representative. Verbatim responses are included to convey the range of perspectives expressed.

When asked how tariffs were affecting their business prior to the policy news, respondents split across three groups. The largest share, six of 18, reported that tariffs had already increased their product costs. Five reported minimal impact. Five said they had been forced to raise prices to customers. Two cited reduced margins.

Immediate Reactions to Policy News

Retail respondent

“I finally feel like we can breathe again.”

Construction respondent

“Hopeful and relieved. Praying for business as usual. Some of the negative changes due to tariffs may not be reversible.”

Professional Services respondent

“Relieved, because economic policy should not be made at the executive branch level. This is an overreach without insight into the unintended consequences for local businesses.”

Food and Hospitality respondent

“I don’t know. If it’s not one thing, it’s another.”

If Tariff Pressure Eases: What Business Owners Would Do

The Broader Sentiment

Import/Distribution respondent

"Anxious, because of uncertainties and instability in global economic markets. Local businesses are the hardest hit, and they are also competing against national corporate brands that have purchasing power that smaller businesses simply do not have."

Summary Statistics

FOR PRESS AND MEDIA INQUIRIES

Revenued Research publishes quarterly data reports on the economic health and outlook of U.S. small businesses. Reporters and editors may cite data from this report with attribution to Revenued.

Full reports and data available at: revenued.com/small-business-reports

Press contact: press@revenued.com

On Shaky Ground: How Small Business Owners Are Navigating Rising Costs, Shrinking Cash, and a Broken Funding System.